Unsecured Business Loans UK: The 2026 Strategic Growth Funding Guide

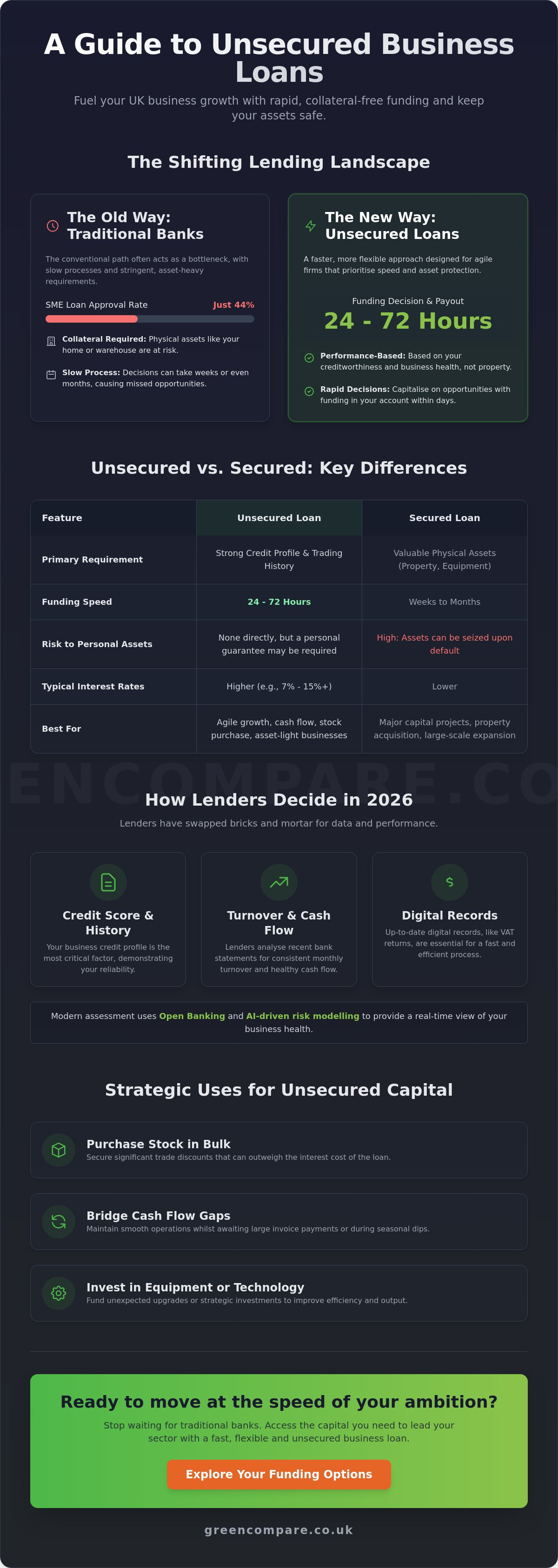

Why wait weeks for a traditional bank to decide your company's future when your competitors are already scaling? With SME loan approval rates recently reported at just 44 percent, the old ways of borrowing often act as a bottleneck rather than a bridge. You need a faster, more flexible approach to unsecured business loans uk to keep your momentum high. We know the stress of managing cash flow gaps whilst waiting for invoices or the fear of risking your personal property just to fund a growth spurt.

It's time to stop viewing debt as a burden and start using it as a high-velocity tool for expansion. You can secure rapid, collateral-free funding to scale your UK business without risking your home or warehouse. This guide shows you how to bypass slow traditional processes and access the capital you need to lead your sector. We'll walk you through the simple application steps, explain the current 2026 lending landscape, and help you retain full ownership of your assets as you move forward. Let's get your business moving at the speed of your ambition.

Key Takeaways

- Learn how to secure capital based on your credit profile rather than your physical property, allowing you to bypass the asset-heavy requirements of traditional banks.

- Discover why unsecured business loans uk are the strategic choice for agile firms that prioritise asset protection and speed in an evolving economy.

- Master the mechanics of fixed-rate funding to ensure your monthly repayments remain predictable whilst you scale your operations.

- Identify the core eligibility criteria and digital record-keeping habits that move your application through the approval process with maximum efficiency.

- Understand how a partnership-led approach to your utilities and finance can create a more resilient and sustainable business model.

Understanding Unsecured Business Loans in the Modern UK Economy

The high-street bank model is struggling to keep pace with the modern UK entrepreneur. In 2026, waiting months for a credit committee to review a thick stack of paperwork is no longer a viable strategy for growth. This is why unsecured business loans uk have become the primary choice for firms that value momentum. Unlike traditional funding, an unsecured loan is capital provided based on your creditworthiness and trading performance rather than physical assets like your home or warehouse. An unsecured loan is a flexible funding instrument for SMEs.

Choosing speed over the absolute lowest interest rate is a pragmatic decision in a fast-moving market. With the Bank of England base rate at 3.75 percent as of February 2026, borrowing costs have stabilised, yet the window of opportunity for business expansion remains narrow. Alternative lenders have filled the gap left by traditional banks, offering agile solutions that match your pace. However, it's vital to remember that "unsecured" does not mean "risk-free". While you aren't pinning your physical assets to the agreement, you are still legally responsible for the debt. Many lenders will still require a personal guarantee to ensure commitment.

The Role of Unsecured Debt in Business Agility

Fast funding allows you to capitalise on sudden market shifts. Whether it's a seasonal stock surge or an unexpected equipment upgrade, having cash in your account within 24 to 72 hours changes the game. Secured debt often involves lengthy valuations and legal checks that can take weeks. By opting for credit-based finance, you maintain your asset liquidity. This keeps your property and equipment free from charges, leaving you with more options for future secured borrowing if you ever plan a major corporate acquisition or property purchase.

Collateral vs. Credit: What Lenders Look For

Lenders have traded bricks and mortar for data and performance. Your business credit score is the most critical factor in this equation. They look at your trading history, VAT returns, and recent bank statements to judge your ability to repay. There are fundamental differences between secured and unsecured business loans that dictate how a lender views your risk profile. Modern assessment processes now use Open Banking to gain a real-time view of your cash flow. This technology replaces the old-fashioned physical valuation, allowing for a decision based on your actual business health rather than the value of your office walls.

The Mechanics of Collateral-Free Financing

Understanding the inner workings of unsecured business loans uk helps you move faster than your competition. Most lenders in 2026 provide funding between £5,000 and £500,000 without requiring a single piece of property as security. This lack of friction is a deliberate design choice. Because no property charges are involved, you completely bypass the heavy valuation fees and legal costs that plague secured borrowing. You can compare the best unsecured business loans to see how rates vary between high-street banks and alternative providers.

Budgeting becomes significantly easier with these products because they almost always feature fixed interest rates. Your monthly repayment remains the same regardless of what happens to the Bank of England base rate during your term. Repayment periods are flexible, typically ranging from six months for quick cash injections to five years for longer-term projects. If you want to see how these products fit your specific budget, you can explore tailored business loans with our team today.

How Lenders Mitigate Risk Without Assets

Lenders in 2026 rely on sophisticated algorithms and AI-driven risk modelling to assess your application in seconds. Since they don't have a building to fall back on, they prioritise your consistent monthly turnover and cash flow health. This higher risk for the lender is reflected in the interest rates. Well-qualified SMEs often see rates between 7 percent and 15 percent, whilst alternative lenders might charge more to accommodate businesses with shorter trading histories. They look for reliability amongst your digital records rather than equity in your home.

Common Uses for Unsecured Capital

The speed of unsecured finance makes it ideal for high-impact business moves. Many UK firms use this capital to purchase stock in bulk, allowing them to secure significant trade discounts that outweigh the cost of the interest. It is also a powerful tool for bridging cash flow gaps whilst awaiting large invoice payments or during seasonal dips. Investing in marketing campaigns, recruitment drives, or technology upgrades are other popular choices. These are the types of investments that generate a rapid return, making the speed of the loan more valuable than a slightly lower rate on a slower secured product.

Unsecured vs. Secured: Navigating Risks and Personal Guarantees

Choosing between secured and unsecured funding is a balancing act between cost and security. A secured loan might offer a lower interest rate because the lender holds a charge over your property or equipment. However, the true cost includes the potential loss of that asset if your business hits a rough patch. For many directors, the emotional peace of mind that comes with ring-fencing the family home is worth the slightly higher APR associated with unsecured business loans uk. You are effectively paying for the protection of your personal and corporate property.

Don't be misled by the word "unsecured." It doesn't mean there is no liability for the borrower. Whilst the lender doesn't take a charge over a specific building, they still need to know you are committed to the repayment. This is where the Personal Guarantee comes into play. According to recent data, around one in three outstanding SME loans in the UK now involves a personal guarantee. It is a standard tool that bridges the gap between your company's credit score and the lender's risk requirements.

The Reality of the Personal Guarantee

A Personal Guarantee (PG) is a legal promise that you will repay the debt from your personal funds if the business cannot. You should distinguish between "limited" and "unlimited" guarantees. A limited guarantee caps your liability at a specific figure, whilst an unlimited version could theoretically cover the entire loan plus interest and costs. To mitigate this individual risk, you can explore PG insurance. This product covers a percentage of your liability, ensuring that a business setback doesn't lead to personal financial ruin. Always review the fine print before signing to ensure your family assets remain protected.

When to Choose Unsecured Over Secured

Speed is often more valuable than the lowest possible interest rate. If you are a service-based firm or a tech startup, you might not even own the physical assets required for a secured loan. In these cases, credit-backed borrowing is your only path forward. For smaller amounts, a government-backed Start Up Loan offers a fixed interest rate of 7.5 percent for sums up to £25,000. This is a prime example of how to secure capital without over-securing the debt. Never pledge a high-value asset, like a £500,000 warehouse, against a small £30,000 loan. It restricts your future borrowing power and places a disproportionate amount of risk on your most valuable property.

Eligibility and Speed: How to Secure Funding in 2026

Speed is the defining characteristic of modern lending. To secure unsecured business loans uk at pace, you must meet a few fundamental hurdles. Most lenders require you to be a UK resident with a business that has been trading for at least six to twelve months. Whilst some government-backed schemes allow for longer windows, private alternative lenders often look for a minimum monthly turnover of £10,000 to £15,000 to prove your cash flow can support the repayments. Organise your records before you hit apply to ensure you don't get stuck in a back-and-forth email chain with an underwriter.

Green Compare acts as your strategic filter in this process. We streamline the search amongst multiple UK lenders to find the most efficient match for your specific sector. This approach is vital because it protects your credit file. If you apply to several banks individually, each one might perform a "hard" credit search. Too many of these in a short period can lower your score and signal desperation to other lenders. We focus on soft searches initially to keep your credit profile pristine whilst we find your best funding fit. To begin your streamlined application, apply for a business loan through our secure platform.

The 5-Step Application Checklist

- Step 1: Gather six months of business bank statements. Most lenders now prefer digital PDF copies or a direct connection via Open Banking for instant verification.

- Step 2: Ensure your latest filed accounts are up to date at Companies House. Lenders will check this first to verify your trading history.

- Step 3: Check your personal and business credit scores. Dispute any errors early, as even a small mistake can trigger an automatic rejection.

- Step 4: Define the exact purpose and amount. Lenders want to see that you have a clear plan for the capital.

- Step 5: Prepare your proof of identity and business address. Have your passport and a recent utility bill ready to pass "Know Your Customer" checks without delay.

Timeline: From Application to Funds in Bank

The transition from "applying" to "growing" is faster than ever. Fintech lenders often provide an instant automated decision based on your credit data and bank performance. If your file is more complex, it moves to the underwriting phase. Here, a human expert reviews your documents to find a way to say "yes" rather than looking for reasons to decline. Once you receive your final offer and sign the digital contract, funds can often be deployed within 24 to 48 hours. This rapid turnaround ensures you never miss a market opportunity because of a slow-moving bank.

Strategic Funding with Green Compare: Empowering Your Business Future

Securing capital is only one half of the growth equation. The other half is ensuring your operational foundation is lean enough to turn that capital into maximum profit. We position ourselves as more than just a finance platform; we are a proactive partner invested in your long-term advancement. By looking at the "whole business," we help you identify efficiencies in your overheads whilst searching for the most competitive unsecured business loans uk. This holistic approach ensures that the funding you receive isn't just plugging a hole, but is actively powering a more sustainable and profitable future.

Our role is to connect you with the right lender, not just the first one that appears in a search result. We understand the pragmatic needs of UK SMEs and the modern entrepreneurial energy required to outpace the competition. We believe in shared progress. When your business scales efficiently, the entire UK economy grows stronger. This visionary outlook drives us to simplify complex financial procedures into linear, actionable steps that respect your time and your ambition.

Why a Comparison Partner Outperforms a Single Bank

Loyalty to a single high-street bank can be a costly mistake for an agile firm. The UK lending market is vast, and a single institution's appetite for risk changes frequently. By using a comparison partner, you avoid the danger of a "no" from your primary bank stalling your progress. We filter dozens of options to match your specific sector and turnover, ensuring you only see offers with a high probability of approval. You can save up to 15 hours of administrative legwork by accessing our panel of lenders through a single, streamlined platform. This efficiency benchmark allows you to focus on your core operations whilst we handle the financial heavy lifting.

Beyond the Loan: Holistic Overhead Management

A strategic loan often works best when paired with lower operating costs. Many of our clients use their capital to upgrade to energy-efficient equipment or technology that reduces their long-term environmental impact. Whilst you are reviewing your finance, it is the perfect time to evaluate your other major overheads. We can help you organise your Business Gas and Business Electricity contracts to ensure you aren't overpaying for your daily operations. Reducing these fixed costs increases your monthly cash flow, making your loan repayments even more manageable. Find your ideal unsecured business loan with Green Compare today.

Power Your Business Growth with Strategic Capital

Unsecured funding is the engine of the modern UK enterprise. You now understand how collateral-free finance protects your personal assets whilst providing the agility needed to seize sudden market opportunities. By prioritising creditworthiness and cash flow over physical property, you maintain the liquidity required for long-term resilience and sustainable expansion. It's about using the right tools to build a more efficient, future-proof business model.

Don't let traditional banking delays or rigid asset requirements hold your vision back. Accessing unsecured business loans uk through a dedicated partner ensures you move at the pace of 2026 commerce. Our platform provides access to a wide panel of UK alternative lenders, with funding decisions often reached within hours rather than weeks. You'll work alongside a UK-based commercial finance specialist who is genuinely invested in your professional advancement and operational success.

Take the next step toward your company's future today. Secure your business growth funding with Green Compare and turn your strategic goals into reality. Your next phase of expansion is within reach; let's build it together.

Frequently Asked Questions

What is the maximum amount for an unsecured business loan in the UK?

Most lenders offer up to £500,000 for unsecured business loans uk, though the specific limit depends on your turnover and credit profile. High-growth firms with strong cash flow may access even higher amounts through specialist alternative lenders. Your capacity to borrow is usually linked to a percentage of your annual revenue to ensure repayments remain sustainable for your operations.

Can I get an unsecured business loan with a poor credit score?

You can still secure funding with a less-than-perfect credit score by approaching alternative lenders who prioritise current cash flow over past mistakes. Whilst high-street banks might decline these applications, specialists look at your recent trading performance to gauge reliability. Expect higher interest rates in these scenarios to reflect the increased risk the lender is taking on your behalf.

How long does it take to get an unsecured business loan approved?

Approval often happens within a few hours thanks to modern fintech algorithms and Open Banking technology. Once you accept the offer and sign the digital agreement, funds can be deposited into your business account in as little as 24 to 48 hours. This speed allows you to act on time-sensitive opportunities without the frustrating delays of traditional banking processes.

Do I always need to sign a personal guarantee for an unsecured loan?

Most lenders require a personal guarantee for unsecured business loans uk to provide an extra layer of security in the absence of physical collateral. This legal commitment ensures that directors are personally responsible for the debt if the business cannot repay. It's a standard practice amongst UK alternative lenders to facilitate faster, asset-free lending for limited companies.

Are interest rates on unsecured loans fixed or variable?

Interest rates for unsecured products are typically fixed for the duration of the loan term. This provides your business with essential certainty, as your monthly repayments won't change even if the Bank of England base rate fluctuates. Fixed rates make it much simpler to forecast your cash flow and manage your growth budget with confidence.

Can a sole trader apply for an unsecured business loan?

Sole traders are absolutely eligible to apply, although the lender will focus heavily on your personal credit history and self-assessment records. Since there is no legal distinction between you and your business, you're personally liable for the debt by default. Many providers offer tailored products specifically designed for the unique needs of self-employed professionals and micro-businesses.

What documents do I need for a fast unsecured loan application?

You generally need six months of recent business bank statements, your latest filed accounts, and valid proof of identity. Having your digital records organised and ready for upload is the best way to ensure a rapid decision from an underwriter. Some lenders may also ask for a brief explanation of how you intend to use the capital to fuel your expansion.

Is there a penalty for repaying an unsecured business loan early?

Early repayment policies vary significantly between lenders, so it's vital to check your specific contract terms before signing. Some agile lenders encourage early settlement and won't charge a penny in penalties, potentially saving you a substantial amount in future interest. Others may require a small fee or charge a portion of the remaining interest to cover their administrative costs.